I had done some studies about Horizon Hill and almost want to ink the deal last weekend but now I decided to give it a miss, at least as for now.

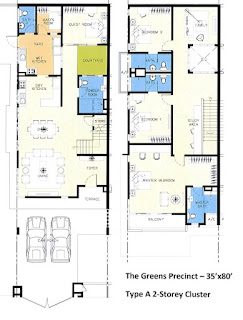

It is a new launch at the Green Precinct. A whopping 35' x 80' size of 2 storey Cluster home. Cluster home is like a semi-detached house without backyard, that's how I name it. The built up area is 3,204 sqft, and land size is 2,800 sqft. Price is RM1,117,800. Beautiful home no doubt. I love the size and the layout.

Let's talk about 90% loan, let's just focus at the first 5 years interest, if you loan 90%, the interest is for only 5 years are whopping close to RM 200,000.

Even though you reduce the loan to 80%, 70% and 60%, the figure are:

80% - interest RM 175,000

70% - interest RM 155,000

60% - interest RM 135,000

For me, it is a self stay property, I don't have rental income of course, and these are the numebrs I must ready to fork out just for the interest. And guess what, the calculation above is using the best rate of 4.1% now, we all know BLR rate can rise and fall, but next chance is going to be UP .

So, if you are buying Horizon Hill for self-stay, take note on the big numbers, even though you are trying very hard to reduce the downpayment to 80%, the number is still RM 175,000 for the first 5 years. Maybe you want to sell the house , then, you also need to take note the real estate property gain tax in Malaysia. The thing is this, you can imagine the property price to shot up , but how much ? Remember, Horizon Hill prices had gone up almost double as 100%, what make you think it will go up another 100% easily. I heard many people said, real estate is an asset to hedge the inflation, but take this example, RM 1.1 mil + 0.2 mil (renovation) + 0.2 mil (interest) = RM 1.5 million after 5 years, my breakeven point is RM 1.5 million ! not to mention the small cost that you need to pay every month. Again, all these money is only for me to enjoy maximum during the weekend only. Because it is the weekend home. I am not going to drive in and out from JB to Singapore every weekday.

Next reason is probably a wise one from my wife.

For those new young couples that are having kids or going to plan to have a kid. Your kids school is important, ESPECIALLY the primary school. I like the west, hence the good school in the West is only Rulang Primary school at Lakeside. I am inspired by my ex-colleague from China, they are Singapore PR, and purprosely bought a flat at block 518, right in front of Rulang primary, and after doing all the volunteer work and some lucks in the ballot, they actually got a seat at the primary school. Such a good news for them. But remember, rules had changed.

As K is going to become Singaporean, and the new Singapore rules is making sure that every single Singaporean kids apply to the particular school must be filled first , or they also need to go through ballot, then if there are still empty seats, it will be Singapore PR ballot time. So, if you are Singapore PR, just don't dream to put your kids into the good school, almost 0% chance. That's one of the tactics that Singapore government force you to become citizen. Your house location is also important !

We are actually thinking either we buy a private condo at Parc Vista, or move our HDB closer to the school, if moving the HDB house, it is almost a No Go to buy a self-stay home at Malaysia now, the rule is once you sell the HDB house, and wanna buy a new one, you have to let go your self-stay home, and of course also my NusaHeights condo, even though it is for rental. So, to buy a HDB near lakeside is fine, in fact, once K becomes citizen, we can also get government subsidised of S$30K to buy another resale flat.

Again, these are all because of my personal commitments and reasons why I give HH a miss, might not be relevant to everybody. As I said, if you buy it for self-stay in JB, and you are driving in and out, that's not a problem, just take note on the interest, and hope that it will become RM 2 million soon... for rental, no comments, as I am not the type of person who want to renovate nicely and rent to others.

For NusaHeights, it is totally different ball games, the rental is enough to sustain the payment + interest, and best of all, the price appreciation had already kicked in. Probably another similar condo investment makes sense for me. For a weekend home for me, I will pause as for now. I am sure Nusa Jaya will be a bright shining star, just plan your financial properly, it's a home anyway, you still need to make sure your spouse, childrens, education, children insurance. I repeat Children insurance, it is very very important, start it young, I will say, start it at age 0, you won't regret it. It is a must.

It is a new launch at the Green Precinct. A whopping 35' x 80' size of 2 storey Cluster home. Cluster home is like a semi-detached house without backyard, that's how I name it. The built up area is 3,204 sqft, and land size is 2,800 sqft. Price is RM1,117,800. Beautiful home no doubt. I love the size and the layout.

The only reason I want to buy Horizon Hill landed residential is to enjoy the lifestyle of spacious green fields and also hope that my parents will stay closer to us rather than staying at Sarawak. I still hope AirAsia is going to launch a direct flight from Sibu to Singapore! So, this investment going to be self-stay, definitely not going for rental. For self-stay, of course it has to be renovated nicely with all the furnitures, that would come be RM150,000-RM200,000 easily based on the size of the house.

So, bear in minds, we have to pay monthly RM 200 for the security, and RM 150 for the facilities usage.

Many of us are able to afford such a home because Malaysia bank is happily giving you a 90% loan as long as you are not holding more than 2 properties in Malaysia (that are still under loan servicing). To buy such a beautiful home, all you need to put is a 10% downpayment, that's RM111,780 plus 3% stamp fees, which is RM 33,534 , total RM 145, 314= SGD 59,000 , we have to convert to Singapore dollars as 70% of the buyers are Singaporean, that's the majority crowds here and the rest of the 30%, most of them are also working in Singapore. So, literally, Horizon Hills are almost filled with people who work in Singapore... so, no doubt, you just need to pay SGD 59K and seal the deal, sound easy. Now, the nightmare comes.

90% loan.

Let's talk about 90% loan, let's just focus at the first 5 years interest, if you loan 90%, the interest is for only 5 years are whopping close to RM 200,000.

Even though you reduce the loan to 80%, 70% and 60%, the figure are:

80% - interest RM 175,000

70% - interest RM 155,000

60% - interest RM 135,000

For me, it is a self stay property, I don't have rental income of course, and these are the numebrs I must ready to fork out just for the interest. And guess what, the calculation above is using the best rate of 4.1% now, we all know BLR rate can rise and fall, but next chance is going to be UP .

So, if you are buying Horizon Hill for self-stay, take note on the big numbers, even though you are trying very hard to reduce the downpayment to 80%, the number is still RM 175,000 for the first 5 years. Maybe you want to sell the house , then, you also need to take note the real estate property gain tax in Malaysia. The thing is this, you can imagine the property price to shot up , but how much ? Remember, Horizon Hill prices had gone up almost double as 100%, what make you think it will go up another 100% easily. I heard many people said, real estate is an asset to hedge the inflation, but take this example, RM 1.1 mil + 0.2 mil (renovation) + 0.2 mil (interest) = RM 1.5 million after 5 years, my breakeven point is RM 1.5 million ! not to mention the small cost that you need to pay every month. Again, all these money is only for me to enjoy maximum during the weekend only. Because it is the weekend home. I am not going to drive in and out from JB to Singapore every weekday.

Next reason is probably a wise one from my wife.

For those new young couples that are having kids or going to plan to have a kid. Your kids school is important, ESPECIALLY the primary school. I like the west, hence the good school in the West is only Rulang Primary school at Lakeside. I am inspired by my ex-colleague from China, they are Singapore PR, and purprosely bought a flat at block 518, right in front of Rulang primary, and after doing all the volunteer work and some lucks in the ballot, they actually got a seat at the primary school. Such a good news for them. But remember, rules had changed.

As K is going to become Singaporean, and the new Singapore rules is making sure that every single Singaporean kids apply to the particular school must be filled first , or they also need to go through ballot, then if there are still empty seats, it will be Singapore PR ballot time. So, if you are Singapore PR, just don't dream to put your kids into the good school, almost 0% chance. That's one of the tactics that Singapore government force you to become citizen. Your house location is also important !

We are actually thinking either we buy a private condo at Parc Vista, or move our HDB closer to the school, if moving the HDB house, it is almost a No Go to buy a self-stay home at Malaysia now, the rule is once you sell the HDB house, and wanna buy a new one, you have to let go your self-stay home, and of course also my NusaHeights condo, even though it is for rental. So, to buy a HDB near lakeside is fine, in fact, once K becomes citizen, we can also get government subsidised of S$30K to buy another resale flat.

Again, these are all because of my personal commitments and reasons why I give HH a miss, might not be relevant to everybody. As I said, if you buy it for self-stay in JB, and you are driving in and out, that's not a problem, just take note on the interest, and hope that it will become RM 2 million soon... for rental, no comments, as I am not the type of person who want to renovate nicely and rent to others.

For NusaHeights, it is totally different ball games, the rental is enough to sustain the payment + interest, and best of all, the price appreciation had already kicked in. Probably another similar condo investment makes sense for me. For a weekend home for me, I will pause as for now. I am sure Nusa Jaya will be a bright shining star, just plan your financial properly, it's a home anyway, you still need to make sure your spouse, childrens, education, children insurance. I repeat Children insurance, it is very very important, start it young, I will say, start it at age 0, you won't regret it. It is a must.

Updated on July 29, 2014

==================

We decided to bring our kid to study at Clementi instead of Lakeside as we had purchased a private residential property at Clementi instead. :)