Senior Principal Engineer, JJ, loves his engineering job and

he intends to work until age 65 and beyond.

His hobby is to write financial blogs, documenting how he builds

a well-diversified retirement portfolio and all the good tricks at any topics

dealing with monies, ranging from credit cards, Singapore Airlines flights,

living cost in Singapore, etc.

Married to an architect, who participated the built of the

Marina Bay Sands Casino, his wife also climbed the corporate ladder further to

Temasek and recently was head hunted to a well-known property developer. They

have a 10 years-old boy, whom JJ had groomed at the age of 3 in Mathematics,

especially. He also pen-downed his teaching experience at his special blog, “Conquering

the Singapore Education System”, showcase only the unique challenging math modeling

questions. He loves to teach as he was a teaching assistant of Circuit Electric

Analysis while he continued his graduate studies in electrical engineering in

Michigan, U.S.A. Not only he collected four full semesters (Fall and Winter

semesters x 2) stipends of US$4,800 each semester, through teaching in the

university, the 2 years graduate school tuition fees were waived too, Teaching

Assistantship. He also conducted private tuition class on campus, charging

US$10 per hour, per student, with a tuition class average of 10 students at one

time. The students were mainly from Middle East rich countries. He graduated

with a 5 digits USD figures in his saving account and landed a job in Singapore

with a Swiss German company specialized in microscopy as a development engineer.

This is the company where he equipped himself with all the precision

engineering skills and he had the opportunity to station at Mannheim, Germany

for one year, responsible for high-end confocal laser scanning microscopy

(CLSM), a new product transfer from Germany to Singapore, whereby the customer

at A*Star research center will pay a million US dollars just for one laser

scanning microscope. During one-year attachment in Germany, not only his basic

salaries in Singapore was untouched, but he was also rewarded a daily oversea allowance

of S$85 a day in Germany. That helped him to save up the first gold bucket very

quickly as a fresh graduate.

Fast forwarded 7 years later, he landed at another Swiss

German DNA company specializing in PCR technology (that was now widely used

during the COVID19 era) and he embarked a honeymoon career as he realized one

must always work as a customer and not a supplier. He went to

Penang regularly (49x trips to be exact) to oversee the production at the

contract manufacturing site to ensure the product quality was met (imagine

working at Apple and oversee the Foxconn iPhone production line). It was an

enjoyable career journey as he had a capable team at Penang.

Life is not always a bed of roses. He was retrenched 7 years

later, on the BREXIT day. There was a massive spin off in Switzerland. He was

rewarded a good retrenchment package, 9 months salaries and he landed another new

career at bio-technology life science American company after 2 months of rest, with

a 30% pay increment and 2 months bonus more than the previous company. He

faithfully works as a R&D engineer until today (the only R&D personnel

in Singapore whereby the hundreds odd of R&D team members are stationed in

India, China, and Chicago).

Who says engineering work is not sexy in Singapore? He

intends to stay for another 23 years in the same company.

Q What’s in your portfolio?

A I invested in equities that are listed in

Singapore, Malaysia, Hong Kong and U.S.A. by using cash account, CPF OA account

and SRS account through POEMS platform. I had invested a good S$600K sum in

equities for long haul, mainly in rock solid blue chips and REITS. I have one fully

paid 4-room resale HDB unit at Toh Guan, currently rented out (rental yield:

11.2%), one 4-bedrooms condominium unit at District 5 for self-stay. I have 2x

private properties at Johor, one FREEHOLD 3-bedrooms unit at Gerbang Nusajaya

(currently rented out at 4% yield) and one 2 bedrooms unit, 129 years leasehold

condominium, at Sunway Iskandar (currently rented out at 3.4% yield). I also

rented out my premium car park lot at Sunway Iskandar for RM100 per month as my

unit is the second highest unit at 35th floor. Amazing, stunning

view up there.

Q What are your immediate investment plans?

A I will not buy any Singapore property now as I do

not want to pay the hefty ABSD charges of 25%. Surely not. Probably, the next

Singapore property purchase will be 14 years later when my son graduates and I

can start buying a new home for him and he will need to pay “monthly mortgage”

to me instead of the bank. That would be a nice, win-win situation.

As we all witness the market correction at USA and China, I personally think it is a great opportunity to start accumulating solid blue chips counters, just to name a few: Amazon, Microsoft, Tencent, Alibaba and index ETF such as SPY (SPDR S&P 500 ETF) and QQQ (Invesco QQQ Trust). I am still buying in different phases.

Q How did you get interested in investing?

A I got inspired by Dr. Y C Chan (Yan Chong) on real

estate rental income. That’s why for my first resale HDB unit, my tenants were paying

my mortgage loan faithfully for years. I stayed in for free.

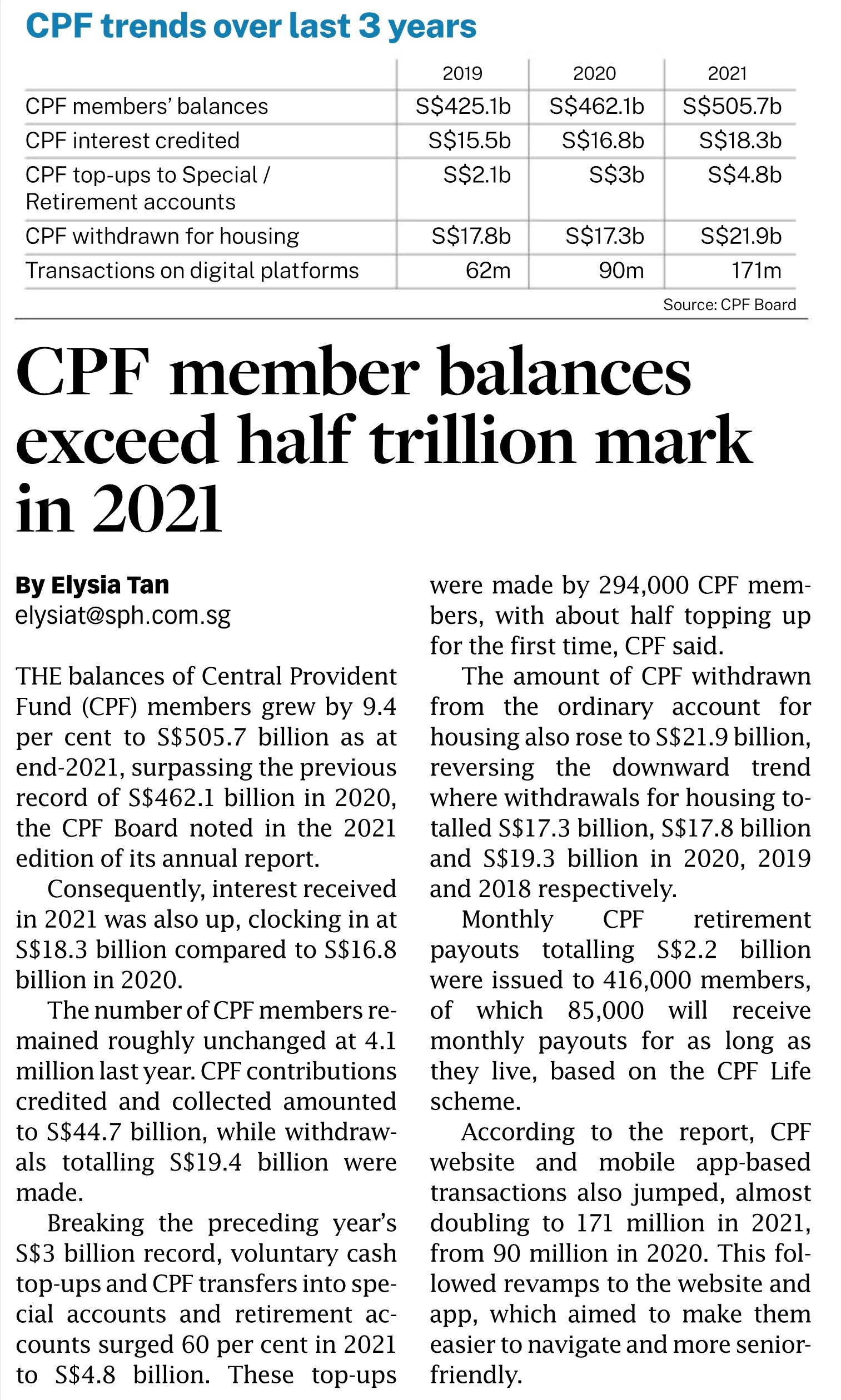

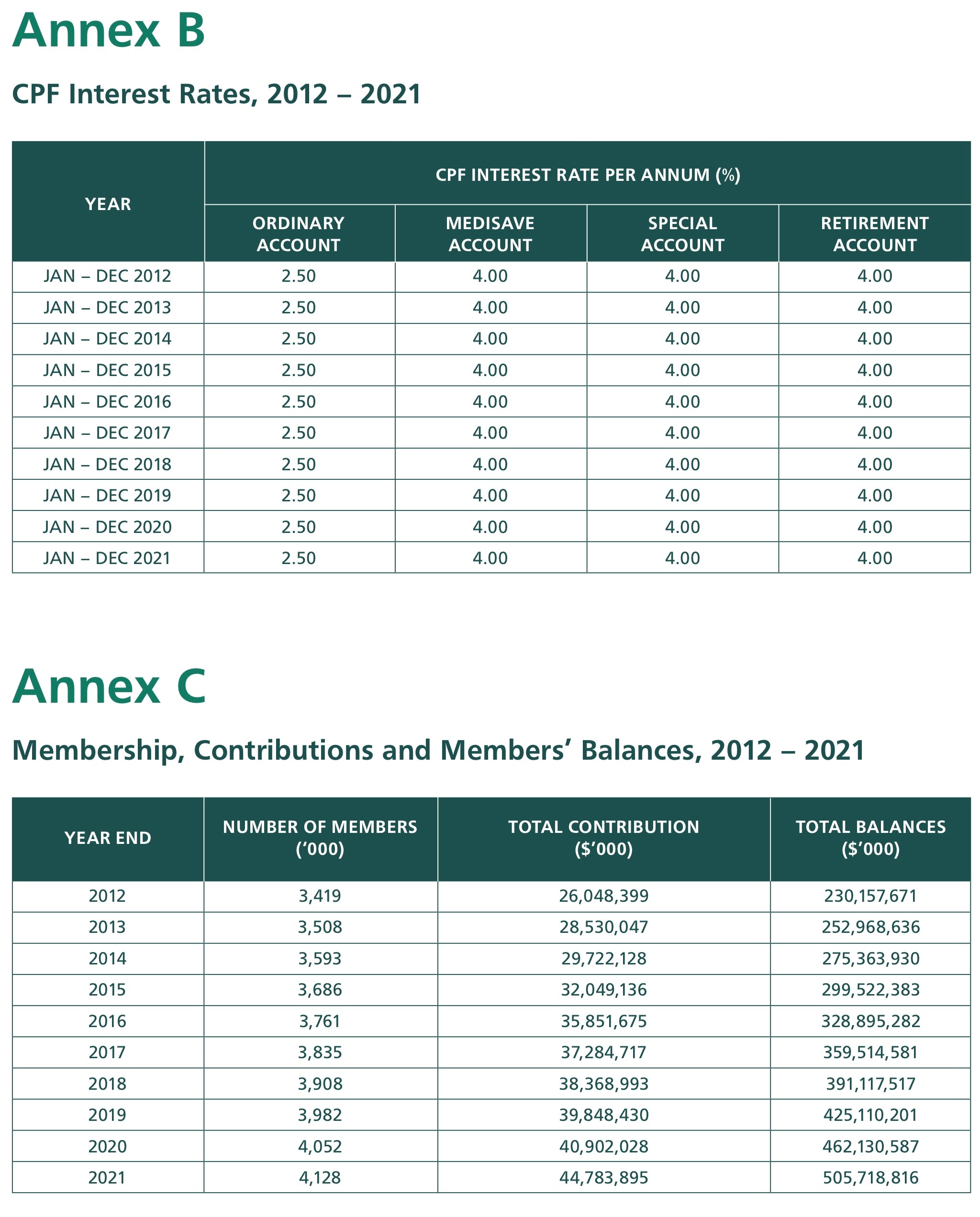

In addition, AK (ASSI) inspired me on CPF, SRS and Singapore

stocks selection. Hence, I max out my FRS in CPF SA account quickly at age 37

together with my wife. AK inspired me to secure the safety net (CPF) strongly

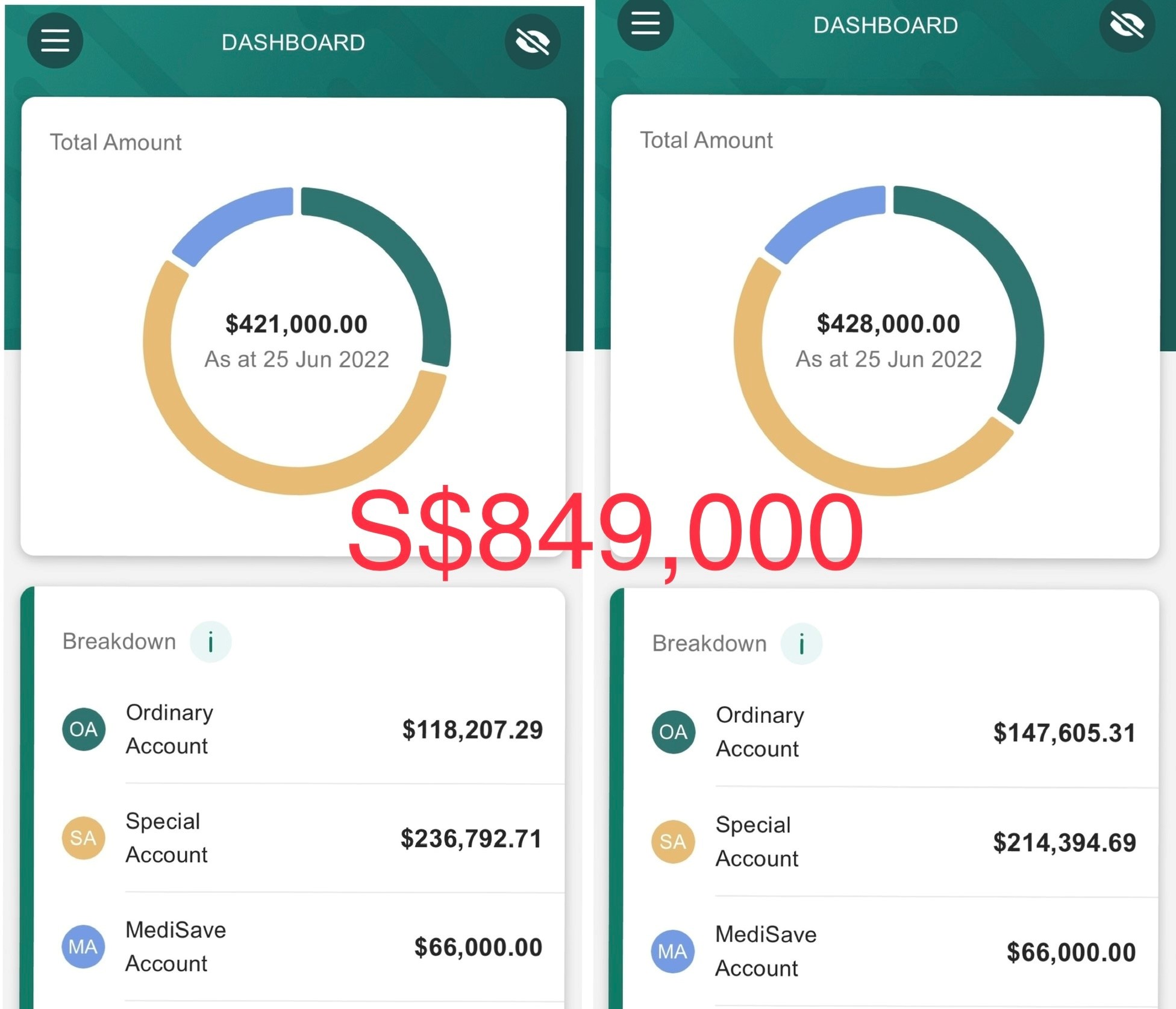

and me and my wife have S$1.134 million in CPF balance (Regrossed Balance) at

the age of 42. Net cash position currently is S$850,000. From now onwards, we will

see our CPF balance jump S$100,000 each year (or S$100,000 jump in each

account every 2 years). Our CPF contribution are on autopilot now. The key

is to stay employed.

Q Describe your investing strategy.

A I am a value investor. I sometimes DCA (dollar cost

averaging) if the price tumbles too quickly while the fundamental never

changes.

I don’t do contra and I don’t short. I also don’t do option

trading.

I now focus on big cap blue chips counters too, e.g., local

banks, Mapletree REITS, Singtel, as well as oversea stocks, DoorDash, Roblox,

Beyond Meat, Airbnb, JD Logistics, WuXi Bio, Genting, etc.

I don’t mind to exposure myself into cryptocurrency with a

small sum, of course, if Bitcoin ever breaks US15,000 level but I do not know

which platform is now safe to buy and hold as there are so many crypto

platforms in deep trouble. Gemini can be a safe one?

Q What else in your financial plan?

A I don’t have term insurance. I don’t have personal

accidental plan too.

I am fully aware of the experts saying, “buy term

insurance, invest the rest”. I will consider term insurance one day, maybe,

if the need arises.

Nevertheless, I have investment linked plan, endowment plan

and whole life insurance plan.

My investment linked plan is from AIA, 100% into Acorns of

Asia fund that is doing well, and I expect to surrender the plan around age 65

during the bull market, not bear market.

Endowment plan is HSBC Target Saver, it will be expired 5

years from now. It will give me pretty much a stable value of S$65,0000. That

is meant for my kid tertiary education fee.

Whole Life insurance plan is TOKIO Marine Legacy plan. It

will be fully paid 4 years later. I plan to keep this plan for my son (to claim

my death benefit) although I also have an option to surrender it at age 65 with

a value of S$350,000.

I also have complete H&S Prudential plan that covers all

my hospital bill. I have never claimed any benefits from this plan thus far and

I count that as a blessing. 3 of us have the complete H&S plan.

Q How are you planning for retirement?

A I will work until age 65. I love my job if all

circumstances stay the same throughout (e.g., the workload and the job

function).

I love to teach. I can conduct Math and Science tuition to

the primary school kids or do a volunteer job at NKF as I know the

technology/business well. I can do part time real estate agent too, not to

mention to travel even more often besides the usual two vacations a year during

the school holidays.

CPF LIFE, SRS and HDB rental income will probably be my

retirement income. Based on 3.5% annual increment in FRS, my FRS sum will be

S$300,800 and that will yield S$2,406 monthly payout. SRS spanning for 10 years

withdrawal, will give me another S$6,000 a month and HDB rental income of

S$3,000 at least will be good for now. Last but not least, my childhood red

packet monies in Malaysia ASNB product, ASM 2 Wawasan, will be a good

sum of RM450,000 (~= S$140K+) when I turn age 65. It was purchased when I was

age 17 with total sum of RM37,000. I probably need to plan to withdraw/

surrender the plan at age 65 too as it will be difficult for Singaporean (my

son) to inherit. I will not convert the Ringgit to SGD as I can spend in

Malaysia whenever I cross over to Johor or back to my hometown at Sarawak

occasionally.

Q Home is now …

A 4 bedrooms condominium at District 5 (Clementi).

My unit is facing the 50m lap pool where I swim 10 laps

almost every day if the weather allows. It is going to be my retirement home. I

like the neighborhood here a lot.

Q I drive …

A 2020 Honda Civic 1.5 Turbo, with CAT B COE

S$41,510. It is a fun car to drive, and I like it.

Worst and

best bets

Q What has been your biggest investing mistake?

A I cut loss in year 2018, S$40,000 loss, in a small cap company. The company changed the name couple of times, maybe 5 times. The chairman is staying at the penthouse of The Sail. It was a stock referred by my ex-colleague and we are still friends.

Q And your best investment?

A It got to be our BLK 286A, 5-room flat at Toh Guan. We bought in late year 2007 and sold in early year 2009. ROI was 390% and IRR was 273% (within 2 years). MOP back then was 1 year.