Revision 03 (last paragraph) : updated on April 10, 2021

Revision 02 (last paragraph) : updated on May 18, 2020

I don't strongly recommend this but this is something extra that I want to do for my baby. We bought a Prudential investment-linked insurance for Micah. It is a Prulink Protection Plus, PruFirst Gift.

Initially, we plan to invest S$200 per month but we reduce to S$100 per month at someone advice. It is because we might be over committed.

With S$100 per month, it has sum assured of S$100,000 for whole life and total & permanent disability coverage for 32 years. Honestly, I forgot why the PD coverage is only 32 years. I have to check with the insurance agent again.

I channel 50% of the funds into PruLink Singapore Growth Fund and the rest of the 50% of the funds into PruLink Emerging Market Fund. It is a good idea to buy with monthly basis because you average out the volatility of the markets. It is definitely not a wise move to buy in yearly mode. Nevertheless, the cost to buy yearly and monthly are the same after all. It is not the same as whole life insurance whereby you have advantage of cost saving if you pay in annual mode. Therefore, don't bother to switch to annual mode payment for investment-linked fund. Your yearly payment date might always catch the wrong cycle in the market, you never know, it is possible.

What is the return? With projected non-guaranteed cash value, with 5% at age 65 (for Micah), it is S$173,900 , with 9% at age 65, it is S$1,122,900 . With the special excel spreadsheet that was given by my agent, I am able to calculate the true yield per annum by keying the annual premium, premium term and final benefits at the certain policy year (it is indeed a powerful spreadsheet). So, effectively, the return is only 2.22% P.A. for S$173,900 at age 65, and 6.44% for S$1,122,900 (S$1 million? Nice !!!! It is possible.) Remember, your kids have another 60 years to play with but not you.

I do agree that the return in per annum basis is nothing fantastic but it shows us the powerful end results of disciplined investment. The disadvantage of all investment-linked fund is you have to keep paying. For our case, that is S$1,200 every year, literally, by age of 65 for Micah, the total payment made by then would be S$78,000.

The reason I pick investment linked is because I want to buy a pool of shares that I believe it will go up greatly in the long run. Singapore and emerging countries are the sectors that I believe it will do very well. If the market situation changes, I can always switch my funds to others region. But I don't think US and Europe will do better. Of course, I also think of instead of buying investment-linked fund, why not just buy the shares directly, for example, buying Citigroup, HSBC every single year until age 65? The problem is I have the tendency to sell the shares after it runs up for 20%. The discipline is hard to control especially when the share goes up in a short time frame. I am also not willing to load up more if the share price keeps going up. Therefore, investment link not only give you the fun of the equities investing, it also provides additional insurance protection for whole life. The table below only shows you the non-guaranteed portion. You will have additional S$100,000 guaranteed benefits on top of all these non-guaranteed cash value.

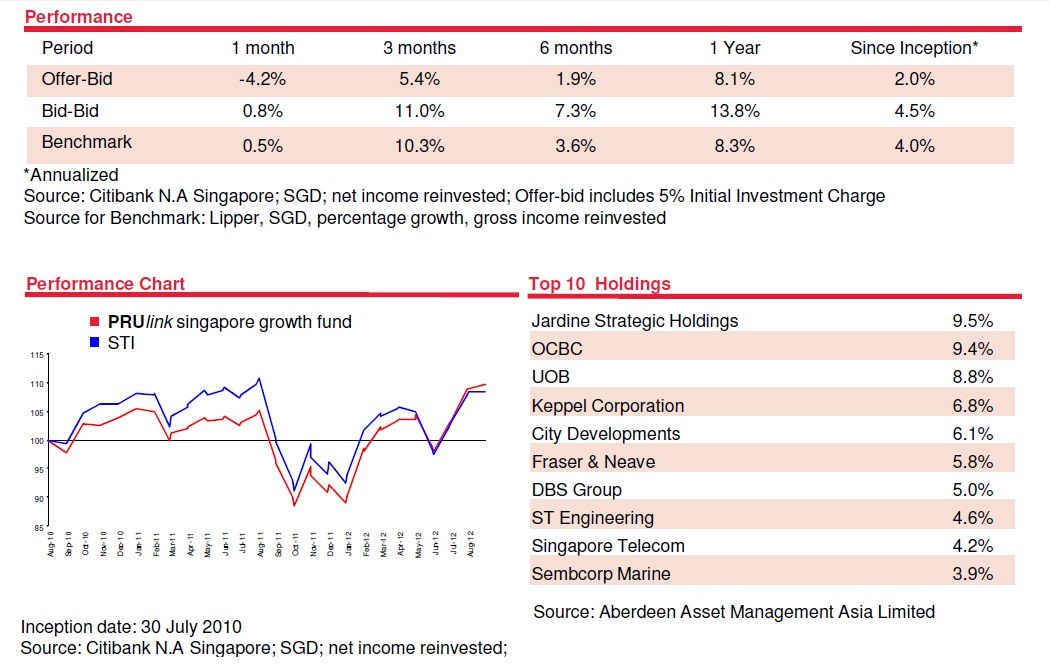

PruLink Singapore Growth Fund:

It is relatively a new fund launched in July 2010. I am surprised that the underlying fund is actually Aberdeen Asset Management Asia Limited. I love all top 10 holdings of this fund, they are all the big local Singapore firms that we can trust (and they give fat dividends) and it occupies 64% of this Singapore growth fund. Great, I love it!

PruLink Emerging markets fund:

This is the risky one, but that is my choice. The underlying fund is JP Morgan Asset Management Limited. The top 5 holdings are Samsung Electronics, Taiwan Semiconductor Manufacturing, China Mobile, etc. If you look at the country allocation of underlying fund, they have pretty equal spreads at China, Brazil, South Korea, South Africa, India, Taiwan, Indonesia and others. These are the countries that I believe they will do well in the next 20 years, if not 40 years ? As for now, the best performing countries in the world now are Indonesia, Thailand and Malaysia (KLSE just hit all time high as for now) !

Prudential products are not cheap, they are well-known for charging higher cost than the rest. But their customer care is super. As for the investment linked products, almost everyone has something to offer, like AIA, HSBC, Mutual Life, Citibank, DBS, UOB, OCBC, Great Eastern, don't be surprised if you see some of the underlying fund are the same! For example, UOB might be selling Prudential products instead.

I am happy that I have settled all the insurance policies for my new born baby. He is only 7 weeks! Now I can focus on other areas.

I have investment-linked fund for myself too. It is AIA Arcons of Asia. I started investing in March 2004 right after I started working in Singapore. They are doing pretty well now. All you need to be aware is, to surrender the policy at the very right timing. I give you one example, if the above Prudential investment linked is surrendered at year 2007, the return will meet the 9% non-guaranteed portion for sure. But if you surrender the policy in year 2009, the return will be only meeting the 5% or even much lower. Hence, the fund that you choose is important and also the timing when you surrender. I will surrender my investment linked policy in the following bull cycle when I am in the age of 50-60, I don't think I can't catch the bull market in a 10 years time frame mentioned above. I should be able to catch it pretty nicely and accurately, by then, STI is 5,000 points ? You bet.

Updated on May 18, 2020

===================

It is good to have an update after 8 years of investing. Are we doing all right ?

Do take note the fund performance update below were dated end March 2020 (Q1 report card), the performance was one of the worst as we had global sell down in March 2020 and it had since rebounded 20-30% from March low.

Let's take a look at the Prulink Singapore Growth Fund first, the fund size has since increased from S$247 millions to S$423 millions (71.3% increase). For the top 10 holdings, we have 2 new comers, namely: CapitaLand and Venture Corporation. They kicked out Sembcorp Marine and Fraser & Neave. The performance are not satisfying, the annualized return for 5 years is barely 0.3%. That's horrible instead but it also created opportunities for us to accumulate low throughout the months now especially we intend to cash out only 60-70 years later (that's when my boy will turn age 68 to 78 ), a good time horizon.

I don't strongly recommend this but this is something extra that I want to do for my baby. We bought a Prudential investment-linked insurance for Micah. It is a Prulink Protection Plus, PruFirst Gift.

Initially, we plan to invest S$200 per month but we reduce to S$100 per month at someone advice. It is because we might be over committed.

With S$100 per month, it has sum assured of S$100,000 for whole life and total & permanent disability coverage for 32 years. Honestly, I forgot why the PD coverage is only 32 years. I have to check with the insurance agent again.

I channel 50% of the funds into PruLink Singapore Growth Fund and the rest of the 50% of the funds into PruLink Emerging Market Fund. It is a good idea to buy with monthly basis because you average out the volatility of the markets. It is definitely not a wise move to buy in yearly mode. Nevertheless, the cost to buy yearly and monthly are the same after all. It is not the same as whole life insurance whereby you have advantage of cost saving if you pay in annual mode. Therefore, don't bother to switch to annual mode payment for investment-linked fund. Your yearly payment date might always catch the wrong cycle in the market, you never know, it is possible.

What is the return? With projected non-guaranteed cash value, with 5% at age 65 (for Micah), it is S$173,900 , with 9% at age 65, it is S$1,122,900 . With the special excel spreadsheet that was given by my agent, I am able to calculate the true yield per annum by keying the annual premium, premium term and final benefits at the certain policy year (it is indeed a powerful spreadsheet). So, effectively, the return is only 2.22% P.A. for S$173,900 at age 65, and 6.44% for S$1,122,900 (S$1 million? Nice !!!! It is possible.) Remember, your kids have another 60 years to play with but not you.

I do agree that the return in per annum basis is nothing fantastic but it shows us the powerful end results of disciplined investment. The disadvantage of all investment-linked fund is you have to keep paying. For our case, that is S$1,200 every year, literally, by age of 65 for Micah, the total payment made by then would be S$78,000.

The reason I pick investment linked is because I want to buy a pool of shares that I believe it will go up greatly in the long run. Singapore and emerging countries are the sectors that I believe it will do very well. If the market situation changes, I can always switch my funds to others region. But I don't think US and Europe will do better. Of course, I also think of instead of buying investment-linked fund, why not just buy the shares directly, for example, buying Citigroup, HSBC every single year until age 65? The problem is I have the tendency to sell the shares after it runs up for 20%. The discipline is hard to control especially when the share goes up in a short time frame. I am also not willing to load up more if the share price keeps going up. Therefore, investment link not only give you the fun of the equities investing, it also provides additional insurance protection for whole life. The table below only shows you the non-guaranteed portion. You will have additional S$100,000 guaranteed benefits on top of all these non-guaranteed cash value.

PruLink Singapore Growth Fund:

It is relatively a new fund launched in July 2010. I am surprised that the underlying fund is actually Aberdeen Asset Management Asia Limited. I love all top 10 holdings of this fund, they are all the big local Singapore firms that we can trust (and they give fat dividends) and it occupies 64% of this Singapore growth fund. Great, I love it!

PruLink Emerging markets fund:

This is the risky one, but that is my choice. The underlying fund is JP Morgan Asset Management Limited. The top 5 holdings are Samsung Electronics, Taiwan Semiconductor Manufacturing, China Mobile, etc. If you look at the country allocation of underlying fund, they have pretty equal spreads at China, Brazil, South Korea, South Africa, India, Taiwan, Indonesia and others. These are the countries that I believe they will do well in the next 20 years, if not 40 years ? As for now, the best performing countries in the world now are Indonesia, Thailand and Malaysia (KLSE just hit all time high as for now) !

Prudential products are not cheap, they are well-known for charging higher cost than the rest. But their customer care is super. As for the investment linked products, almost everyone has something to offer, like AIA, HSBC, Mutual Life, Citibank, DBS, UOB, OCBC, Great Eastern, don't be surprised if you see some of the underlying fund are the same! For example, UOB might be selling Prudential products instead.

I am happy that I have settled all the insurance policies for my new born baby. He is only 7 weeks! Now I can focus on other areas.

I have investment-linked fund for myself too. It is AIA Arcons of Asia. I started investing in March 2004 right after I started working in Singapore. They are doing pretty well now. All you need to be aware is, to surrender the policy at the very right timing. I give you one example, if the above Prudential investment linked is surrendered at year 2007, the return will meet the 9% non-guaranteed portion for sure. But if you surrender the policy in year 2009, the return will be only meeting the 5% or even much lower. Hence, the fund that you choose is important and also the timing when you surrender. I will surrender my investment linked policy in the following bull cycle when I am in the age of 50-60, I don't think I can't catch the bull market in a 10 years time frame mentioned above. I should be able to catch it pretty nicely and accurately, by then, STI is 5,000 points ? You bet.

Updated on May 18, 2020

===================

It is good to have an update after 8 years of investing. Are we doing all right ?

Do take note the fund performance update below were dated end March 2020 (Q1 report card), the performance was one of the worst as we had global sell down in March 2020 and it had since rebounded 20-30% from March low.

Let's take a look at the Prulink Singapore Growth Fund first, the fund size has since increased from S$247 millions to S$423 millions (71.3% increase). For the top 10 holdings, we have 2 new comers, namely: CapitaLand and Venture Corporation. They kicked out Sembcorp Marine and Fraser & Neave. The performance are not satisfying, the annualized return for 5 years is barely 0.3%. That's horrible instead but it also created opportunities for us to accumulate low throughout the months now especially we intend to cash out only 60-70 years later (that's when my boy will turn age 68 to 78 ), a good time horizon.

Nevertheless, the Prulink Emerging Markets fund is doing very well. The annualized return for 5 years had reached 4.3% even though it also experienced the massive sell down in March 2020. They re-shuffled the top 5 holdings. The fund manager did a great job to include Alibaba, Tencent, AIA and HDFC India bank. They kicked out Samsung Electronics, China Mobile, Housing Development Finance and CNOOC. I think they had made a right move. I personally think Alibaba and Tencent will continue to do well in the next 10-20 years. They should hold them for long.

It is also good to check out the past 8 years fund price movement.

For Singapore Growth fund, the March 2020 sell down touched the rock bottom price level created in January 2016 too. As for the peak in Feb 2018, it has a price appreciation of 38% based on my first entry in October 2012.

For Emerging Market fund, the bottom was also created in January 2016 and it had a peak in January 2020. That was right before COVID 19 escalated globally. It has a price appreciation of 65% based on my first entry in October 2020.

After all, I still believe both funds will perform well in the long term. Let's look at the performance again 8 years later ! : )

Updated on April 10, 2021

====================

====================

Just after 1 year, both funds rebounded sharply!

The information below were updated on Feb 28, 2021.

For PRUlink Singapore Growth fund, they trimmed down the stakes on Jardine Strategic Holdings, City Developments and Keppel Corporation. Capitaland Mall Trust (CICT) 3.6% , IFAST Corporation 2.5% and Nanofilm Technologies 2.4% are now part of the members of top 10 holdings.

The fund touched low at $1.00 level in March 2020 and rebounded 50% to $1.50 in April 2021.

For PRUlink emerging markets fund, Samsung Electronics 5.0%, Sea 3.5% are the new members of top 5 holdings, replacing AIA and HDFC.

The fund also touched low at S$1.45 in March 2021 and rebounded 100% to S$2.90 in February 2021.

Amazing run indeed. :)

No comments:

Post a Comment